Clicking "Apply" inside your Tesla app feels like the fastest route to your new Model 3 or Model Y, but that convenience could be a costly trap. While manufacturer tesla finance seems like the path of least resistance, the most obvious choice often isn't the one that keeps the most cash in your pocket.

We know the feeling. You’ve nailed the car's configuration, but now you're facing a wall of complex FBT rules and confusing balloon payment options. It's stressful when slow bank approvals threaten to blow your delivery window. You deserve a finance structure that’s as high-performance as the car itself, particularly with the full FBT exemption set to change after 31 March 2027.

This article shows you how to secure the most cost-effective and flexible loan for your EV. We'll compare manufacturer offers against tailored broker solutions to find the best fit for your budget. You’ll learn how to navigate the $91,661 luxury car tax threshold and lock in a tax-optimised deal with the lowest possible monthly repayments.

• Understand why Tesla’s direct-to-consumer model requires you to organise your own funding before your delivery window opens.

• Compare the "One Lender" manufacturer approach against a multi-lender model to secure the most competitive tesla finance for your specific credit profile.

• Discover how to leverage the FBT exemption for vehicles under the $91,661 Luxury Car Tax threshold to slash your monthly repayments.

• Learn why a tailored business loan or novated lease structure often provides superior tax benefits compared to a standard bank loan.

• See how a streamlined three-step approval process can get you behind the wheel faster without the typical bank bureaucracy.

Buying a Tesla isn't like visiting a traditional dealership. There's no suit-clad finance manager waiting in a back office to run your credit. Instead, the "Tesla Direct" model puts you in the driver’s seat of the entire process. This means tesla finance is a collection of different funding pathways you need to organise yourself. These range from chattel mortgages for business owners to consumer loans and novated leases for individuals.

By 2026, the Australian market has matured significantly. Lenders now have years of data on Tesla resale values, which makes them more comfortable offering competitive rates. Many now offer "Green Loans" specifically for EVs. These products often feature lower interest rates than standard car loans because lenders want to incentivise sustainable choices. It's a key part of the broader Australian electric vehicle policies designed to get more zero-emission cars on our roads.

Your choice depends on how you'll use the car. A personal loan is straightforward for daily commuting. However, if you're using the Tesla for work, commercial finance through a chattel mortgage is often the smartest play. This structure allows eligible businesses to claim the GST on the purchase price upfront. It’s a massive cash flow win that standard consumer loans just can't match.

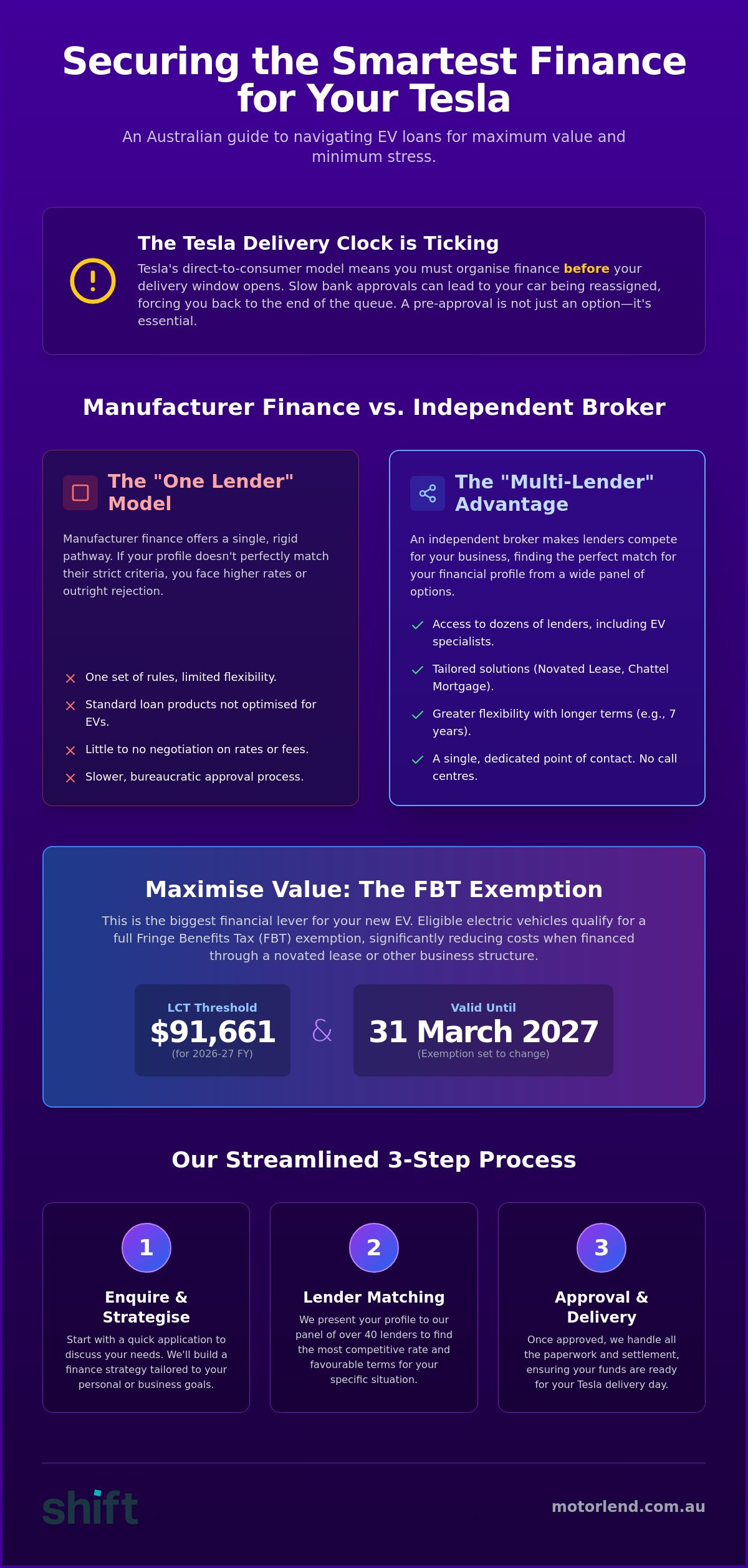

Tesla operates with brutal efficiency. Once your car is assigned a VIN (Vehicle Identification Number), the clock starts ticking. If your finance isn't ready when you get that "Ready for Delivery" alert, Tesla might reassign your car to the next person in line. Securing a vehicle finance pre-approval is vital. It keeps you ready to move the moment your app updates. Don't risk losing your VIN assignment because of slow bank paperwork.

Choosing between manufacturer tesla finance and an independent broker is the difference between a "one size fits all" suit and a tailored one. Tesla and the big banks use a "One Lender" model. They have one set of rules and one bucket of money. If you don't fit their specific box, you're often stuck with a higher rate or a flat rejection. It's rigid and doesn't account for your unique financial situation.

A broker uses a "Multi-Lender" model. We find the specific lender that has an appetite for your credit profile. This is crucial because every lender views risk differently. We can often negotiate or waive the "standard" application fees that big banks keep as a default. It's about making the lenders compete for your business, not the other way around.

Big banks are often slow to move. They frequently treat an EV loan exactly like a standard petrol car loan. We work with non-bank lenders who specialise in electric vehicle residuals. They understand that a Tesla holds its value differently than a traditional car. You also get a single point of contact at Motorlend. No call centres. No waiting on hold for an hour. Whether it's a Model Y or other vehicle finance, we manage the entire process from application to settlement.

Flexibility is where we really shine. Most banks cap their terms at five years. We can often secure 7-year terms to bring those monthly repayments down significantly. We also help you structure balloon payments to maximise the ATO Electric Car FBT Exemption. This keeps more cash in your pocket for other investments. If you want to see what's possible for your situation, you can start your application today and get a clear picture of your options.

The biggest financial lever you can pull for your new EV is the federal Fringe Benefits Tax (FBT) exemption. For the 2026-2027 financial year, any eligible electric vehicle with a value below the $91,661 Luxury Car Tax (LCT) threshold qualifies. This exemption remains in full effect until 31 March 2027. It effectively turns a standard tesla finance package into a high-performance tax strategy. By using a novated lease or a specific commercial structure, you're paying for the car and its running costs with pre-tax income. This can slash your taxable salary and put thousands back in your pocket every year.

While state-based rebates have largely phased out across Australia by 2026, federal incentives have stepped up. The key is staying under that $91,661 ceiling. If you spec up a Model 3 Performance or a Model Y with too many premium options, you might accidentally cross the threshold and lose the entire FBT benefit. We help you crunch those numbers before you hit "order" to ensure your tesla finance stays tax-optimised and eligible for every available cent in savings.

We don't just find a rate; we find a structure. We often talk directly with our clients' accountants to ensure the loan aligns with their broader tax goals. Many Australian lenders now offer "Green Finance" specifically for EVs. These products often come with interest rates significantly lower than standard personal loans. It's a reward for going electric that most big banks don't advertise upfront. We know which lenders have the strongest appetite for EV debt right now.

Teslas are known for their strong resale value compared to traditional internal combustion vehicles. This market strength allows for more aggressive balloon payments. By setting a higher residual value at the end of the term, you can keep your monthly cash flow high for other investments. If you're unsure how this works, check out our Balloon Payments Explained guide for a full breakdown.

Ready to maximise your savings? Apply for your tailored quote here and let's get your Tesla on the road with a structure that works for you.

Securing your tesla finance shouldn't feel like a part-time job. We've stripped away the banking bureaucracy to create a streamlined three-step process: Consultation, Comparison, and Fast Approval. We start by understanding your specific needs, whether you're a high-mileage commuter or a small business owner. From there, we scan our panel of lenders to find the one that offers the best fit for your credit profile. Once we've found the winner, we move straight to securing an approval that aligns with your delivery date.

Our "No-Nonsense" approach means we handle the tedious paperwork on your behalf. You shouldn't have to spend your lunch break chasing bank managers or deciphering fine print. We also offer the flexibility to bundle your Tesla Wall Connector and other factory accessories directly into your loan. It’s a simple way to manage your total EV investment under one competitive rate without dipping into your savings for the home charging setup.

Tesla’s delivery windows are notoriously tight once a VIN is assigned. Our team has specialist knowledge of these cycles, ensuring your funding is ready the moment your app says "Ready for Delivery." This prevents the common heartbreak of reassigned vehicles due to finance delays. We're committed to finding the most competitive rate across our extensive panel of lenders to ensure your loan is as efficient as the car you're driving.

Don't settle for the first offer you see in your app. A quick five-minute chat with a broker can often save you thousands of dollars over the life of your loan. We're here to make the process fast, transparent, and completely stress-free. Visit our online application page now to get a quick quote before you hit "Confirm" on your order.

You’ve done the research on the car; now it’s time to ensure the numbers are just as impressive. Choosing the right tesla finance isn't just about getting an approval. It’s about matching your loan to the 2026 tax landscape. Whether that’s staying under the $91,661 LCT threshold to keep your FBT exemption or structuring a balloon payment that protects your cash flow, the details matter. A tailored approach ensures you don't leave money on the table when you drive away.

Don’t risk losing your VIN assignment by waiting for a slow bank approval. Our team offers fast, local service and access to over 30 leading Australian lenders who specialise in EV and Green Finance tax structures. We know the Australian market inside out and we're ready to help you skip the bureaucracy. We handle the heavy lifting so you can focus on the delivery date.

Ready to see what you could save? Get a tailored Tesla finance quote from Motorlend and secure a deal that’s as high-performance as your new drive. It’s time to get behind the wheel with total confidence and a structure that works for your budget.

Yes, you can definitely secure finance as a self-employed individual. Most of our lenders offer Low Doc or No Doc loan options specifically for ABN holders who have been trading for at least 12 months. This means you won't always need full tax returns to get an approval. We specialise in matching business owners with lenders who understand the unique cash flow of the self-employed market.

An independent broker generally offers more choice and better rates than a manufacturer's preferred financier. While Tesla’s in-app experience is simple, it only represents one lender's rigid criteria. A broker creates competition by comparing dozens of tesla finance products. This often leads to lower interest rates and more flexible terms tailored to your specific credit score and financial goals.

The maximum loan term for a Tesla in Australia is typically seven years. While many big banks try to limit car loans to five years, our panel of lenders offers longer terms to help keep your monthly repayments manageable. A seven-year term can be a great way to improve your weekly cash flow; especially when combined with a structured balloon payment at the end.

The FBT exemption significantly reduces your effective loan cost by allowing you to pay for the car using pre-tax salary. If your Tesla is priced under the $91,661 Luxury Car Tax threshold, you can save thousands in tax every year. This structure makes tesla finance through a novated lease much cheaper than a standard car loan because it lowers your taxable income while covering all running costs.

No, you don't necessarily need a deposit to secure funding in 2026. Many of our lenders offer 100% finance options for both personal and business applicants with a strong credit profile. This allows you to keep your cash in your pocket or offset account while still getting behind the wheel. We can help you determine if a "no deposit" loan is the right move for your specific financial situation.