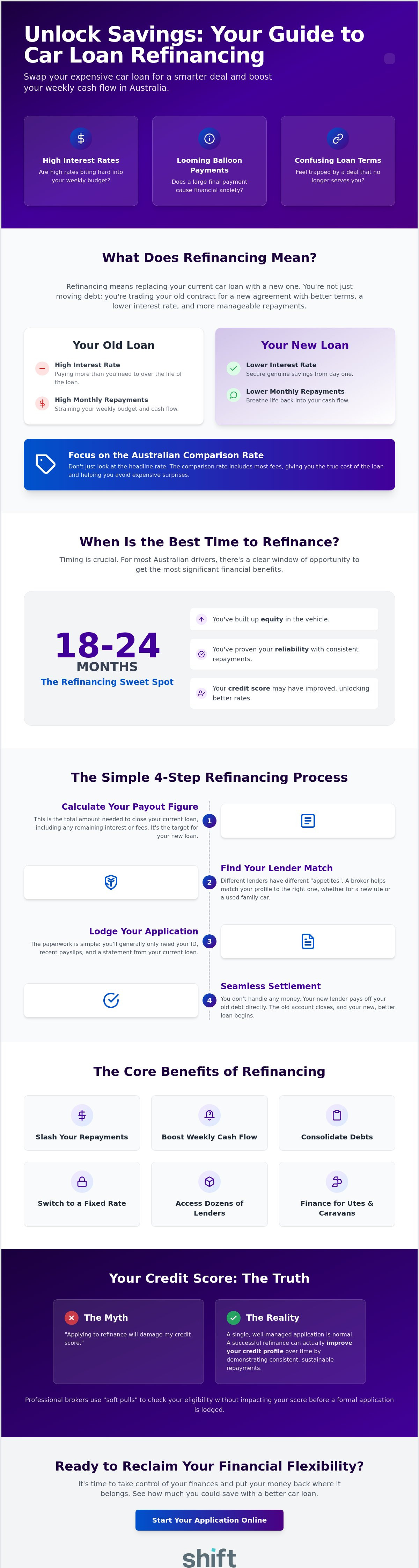

Why keep paying a premium when the average car loan rate for property owners has settled at 7.65% this June? If you want to refinance car loan, you've likely noticed that high interest rates are biting hard into your weekly budget. It's frustrating to feel trapped by a deal that no longer serves you, especially when confusing exit fees and "bank-speak" make switching feel like a chore.

We know that financial anxiety often stems from that looming balloon payment or a loan term that's just too tight. You deserve a repayment plan that breathes life back into your cash flow. This guide promises to show you exactly how to slash your monthly costs and secure a far more competitive rate. We'll preview the best 2026 strategies to dodge hidden fees and explain how getting the right help can make the entire process stress-free. It's time to take control of your finance and put your money back where it belongs.

• Swap your high-interest debt for a fresh agreement designed to boost your weekly cash flow and lower your monthly repayments.

• Identify the 18-to-24-month "sweet spot" when switching lenders often yields the most significant financial benefits for Australian drivers.

• Learn how to accurately assess your current payout figure to ensure your new loan delivers genuine savings from day one.

• Discover why using a broker to refinance car loan provides access to dozens of lenders that big banks simply can't offer.

• Find out how to secure tailored finance for utes, commercial vehicles, or leisure assets like caravans that fit your unique financial profile.

•

What Does it Mean to Refinance a Car Loan in?

•

How the Refinancing Process Works in 2026

•

When is the Best Time to Refinance Your Vehicle?

•

Securing a Better Deal: Why Use a Finance Broker?

At its simplest, to What Does it Mean to Refinance your vehicle is to take out a fresh loan to pay off your existing one. You aren't just moving debt; you're trading in your old contract for a new agreement that better suits your life today. If you choose to refinance car loan, you're essentially asking a new lender to clear your current "payout figure." This gives you a clean start with terms that actually align with your current financial goals and credit score.

Don't get caught out by the headline rate alone. While a low interest rate looks great on a billboard, the** Comparison Rate** is what really matters. It includes the interest plus most upfront and ongoing fees, giving you the true cost of the loan. In a market where some distributor establishment fees can reach $2,500, looking only at the headline rate is a mistake that could cost you thousands over the journey.

Even a modest 1% or 2% drop in your interest rate can save you a significant amount over the life of a loan for a standard family SUV or a work ute. By exploring different Vehicle Finance Options, you can instantly reduce your monthly repayments and keep more cash in your pocket. Some drivers also choose to extend their loan term to improve their weekly cash flow, though you should always weigh this against the total interest paid over the longer period.

Refinancing is a tactical move that offers more than just a lower rate. You can use it to roll smaller, high-interest debts into one manageable monthly payment, simplifying your life. Many Australians are also switching from variable rates to fixed rates to lock in budget certainty while the economy fluctuates. In the 2026 market, car loan refinancing serves as a high-performance tool for reclaiming your financial flexibility and outmanoeuvring rising costs.

The path to a better deal is much faster than it used to be. You don't need to spend hours buried in paperwork or waiting on hold with banks. To refinance a car loan, the process has been refined into a quick, four-step sprint. It starts with your payout figure. This is the total amount needed to close your current loan today, including any interest or fees. Knowing this number is essential because it sets the target for your new finance agreement.

Next, you match your financial profile with a new lender. Every bank has different "appetites" for risk; some prefer brand-new utes while others specialise in used family cars. Understanding how car loans work in Australia can help you spot which lender criteria align with your situation. Once you find a match, the application phase is straightforward. You'll generally only need your ID, recent payslips, and a statement from your current loan.

The final stage is settlement. This is the best part because you don't actually have to handle the money yourself. Your new lender pays off your old debt directly. The old account closes, and you're left with a fresh agreement that has a lower rate and more manageable repayments. It's a seamless transition that happens mostly in the background.

Many people fear that looking for a better deal will damage their credit score. While submitting five formal applications at once is a mistake, a single enquiry for a refinance is perfectly normal. Professional brokers often use "soft pulls" to check your eligibility before a formal application is even lodged. A successfully refinanced loan can actually improve your credit profile over time by proving you can consistently meet a more sustainable repayment schedule.

Lenders look for stability and value. Most secured refinancing options have a vehicle age cut-off, usually around 10 to 12 years old. If your car is newer and you've maintained a clean repayment history on your current loan, you're a prime candidate for a better rate. If you're curious about your options, you can start your application online to see how much you could save.

Timing your move is just as important as finding the right rate. For many Australian drivers, the 18 to 24 month mark is the absolute sweet spot. By this stage, you've likely built up some equity in the vehicle and proven your reliability to lenders through consistent repayments. If your credit score has climbed since you first drove off the lot, you're in a prime position to refinance a car loan and secure a more competitive deal.

Life changes are another major trigger for a better deal. Perhaps you've landed a significant pay rise or moved from a casual role to a stable, full-time position. Lenders value this stability and may offer much lower rates than what you received when your circumstances were different. Before you switch, always calculate your "break costs." If the monthly savings from a lower interest rate outweigh the exit fees of your old loan within a few months, it's a green light to move. Sometimes, exploring Personal Loans for Refinancing can provide the flexibility you need if your vehicle's value or your needs have changed.

A massive 30% or 40% lump sum due at the end of your term can cause serious financial anxiety. This "balloon trap" often catches people off guard when they realise they don't have the cash sitting in the bank. Instead of a massive outlay, you can refinance that balloon into a new, smaller loan with manageable terms. We recommend organising your finance at least three months before the due date to ensure a smooth transition. To learn more about managing these costs, check out our guide on how to Avoid Hidden Balloon Payments.

Don't let the fear of exit fees stop you from saving money. While older loans might use the "Rule of 78" to front-load interest, most modern Australian loans use simpler, more transparent fee structures. The easiest way to cut through the confusion is to ask your current bank for a "Letter of Payout." This document shows the exact amount needed to close the account today. If the numbers stack up and the savings are clear, you can apply for a better rate today and start keeping more of your hard-earned money.

When you walk into a big bank, they have exactly one option for you. It's their way or the highway. But when you choose to refinance a car loan through a broker, the power shifts back to you. You gain instant access to dozens of lenders who are actually competing for your business. It isn't just about finding any loan. It's about finding the exact match for your specific vehicle and budget.

Brokers understand that every borrower is different. Some lenders specialise in work utes and commercial vehicles, while others are the best choice for leisure assets like caravans or motorhomes. We handle the stressful back-and-forth with credit managers so you don't have to. Because we have established relationships, we can often fast-track applications that might otherwise stall in a bank's bureaucracy. It's a no-fuss factor that lets you focus on your life while we do the heavy lifting.

Don't limit yourself to the Big Four banks. Tier 2 and Tier 3 lenders often have much more competitive refinance rates because they are hungrier for your business. They also have policy niches that allow them to be more flexible. If you want to refinance a car loan, these lenders are often your best bet, especially if you're self-employed or have a unique income type that doesn't fit a standard bank's rigid box.

We pride ourselves on being more than just a middleman. Our expertise spans everything from standard vehicle finance to complex commercial and leisure asset loans. We believe in straight-talking Australian service with zero hidden catches. Our goal is simple: to get you a better deal with the least amount of fuss possible. We value your time and work hard to ensure the process is as smooth as your next drive.

Ready to see how much you could save? Apply for a refinance quote today.

Lowering your monthly repayments isn't just a dream; it's a tactical move that savvy drivers are making right now. By understanding the comparison rate and timing your move around the 18-to-24-month mark, you can reclaim your weekly budget from high interest rates. Whether you are staring down a looming balloon payment or simply want a better deal, the path to financial relief is clearer than ever.

Choosing to refinance a car loan wide with a specialist means you don't have to settle for what one big bank offers. Motorlend provides a no-nonsense, expert brokerage service that cuts through the red tape. We give you access to over 30+ lenders, specialising in everything from standard vehicle finance to leisure asset finance like caravans and motorhomes. Let us handle the paperwork and the bank negotiations while you focus on your life.

Get a fast, obligation-free refinance quote with Motorlend and see exactly how much you could save. It's time to stop overpaying and start driving a better deal today.

It can definitely be worth it if the interest savings over those final 24 months exceed any exit fees from your current lender. Even a small rate drop can shave hundreds off your remaining debt; providing immediate relief to your weekly budget. You'll need to compare your current total cost against the new comparison rate to see the real benefit before making the switch.

You can certainly refinance a balloon payment to avoid a large cash outlay at the end of your term. This process involves taking out a new loan to cover the residual value; effectively turning that lump sum into smaller, regular repayments. It's a smart way to keep your car without draining your savings all at once; especially if you plan on keeping the vehicle for several more years.

A single application to refinance a car loan will usually cause a minor, temporary dip in your credit score due to a hard enquiry. However, consistently meeting your new, lower repayments can actually strengthen your credit profile over the long term. Professional brokers often use "soft pulls" to check your eligibility first; which helps protect your score from unnecessary damage before a formal application is lodged.

The total cost usually involves "break costs" from your old lender and establishment fees for the new agreement. Industry data shows that lender establishment fees often range from $299 to $995; while broker or distributor fees can vary depending on the complexity of the deal. The goal is always to ensure your total interest savings are significantly higher than these upfront charges so the move makes financial sense.

It is possible to move from a secured loan to an unsecured one; though this usually depends on your credit strength and the vehicle's current value. Unsecured loans often come with slightly higher interest rates because the lender has no asset to claim if you stop paying. Most Australian drivers prefer staying with a secured loan to keep their interest costs as low as possible while benefiting from a fresh agreement.