That low interest rate you saw on a billboard is likely a marketing myth designed to get you through the dealership door. It's frustrating when the "from" rate doesn't match the quote you actually receive. Most Aussies feel the sting of "sticker shock" when personalised car finance rates turn out higher than advertised, or when hidden fees and balloon payments start creeping into the fine print. Dealing with pushy finance managers shouldn't be part of the car-buying experience.

You deserve a clear path to your next vehicle without the stress or the bank's endless red tape. We've designed this guide to help you navigate the 2026 lending landscape, compare the big banks against specialised brokers, and secure a finance package tailored to your specific budget. We'll break down the latest market data, explain how risk-based pricing affects your repayments, and provide a simple comparison framework to ensure you drive away with a genuine win.

• Understand how the 2026 economic climate and RBA shifts directly impact the cost of borrowing for your next motorised asset.

• Learn how to use your credit health to unlock better car finance rates and avoid the "sticker shock" of advertised versus personalised quotes.

• Compare the rigid criteria of big banks against the convenience of dealers to find the most cost-effective way to fund your car.

• Get a clear comparison framework to help you spot hidden fees and navigate complex balloon payment structures with confidence.

• Discover how a specialised broker simplifies the approval process for everything from daily drivers to weekend caravans and boats.

At its simplest, a car finance rate is the price you pay to use someone else's money to get behind the wheel. In 2026, that price has been a moving target. The Reserve Bank of Australia (RBA) has kept everyone on their toes, with cash rate shifts driving average car loan interest rates up by more than 0.50 percentage points in the first half of the year alone. Understanding how car finance works in this environment means looking beyond the flashy percentages you see on social media ads.

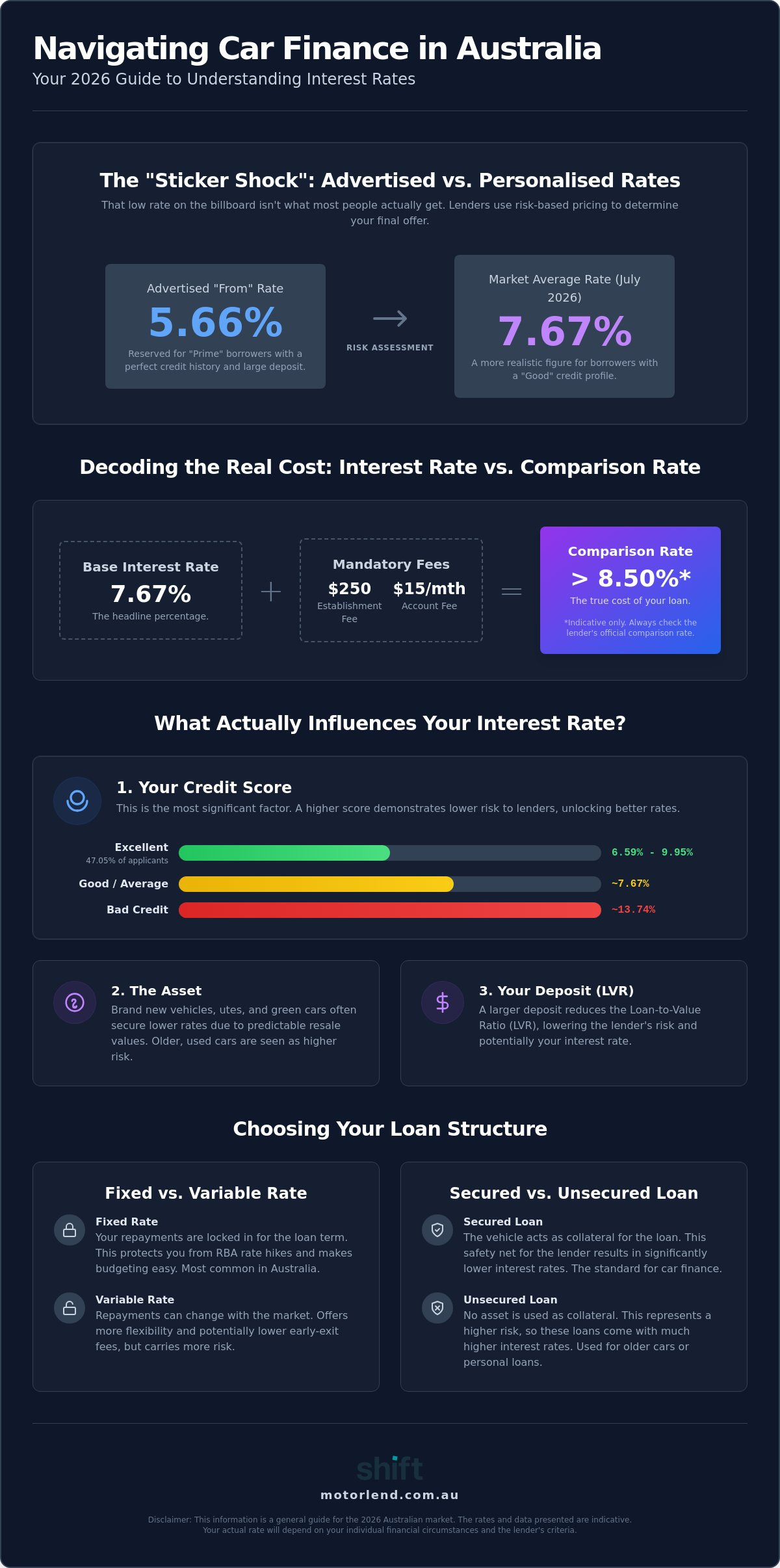

While the base interest rate is what you'll see in big bold text, it's the comparison rate that tells the real story. This figure includes the interest plus most upfront and ongoing fees, like the $250 establishment fees or $15 monthly account fees common with major lenders. The comparison rate is the only figure that reveals the true total cost of your loan by bundling the interest rate with mandatory fees and charges.

That 5.66% rate you spotted online? It's likely reserved for "Prime" borrowers with a spotless credit history and a large deposit. Lenders use risk-based pricing to sort applicants into tiers. If your credit score is "Good" rather than "Excellent," you might find car finance rates closer to the July 2026 market average of 7.67%. Your personalised rate is a reflection of your unique financial footprint, not just a generic market number.

Most Aussies opt for a fixed rate when securing vehicle finance. It locks in your repayments for the life of the loan, protecting you from any further RBA hikes. It's the "set and forget" approach that makes budgeting easy. Variable rates are rarer in the car world but offer flexibility if you plan to pay the loan off early without the early exit fees that some fixed contracts carry. Pick the one that lets you sleep better at night.

Why does one person get a lower rate than their neighbour for the exact same car? It's all about risk. Australian lenders use a complex set of criteria to determine how likely you are to repay the loan on time. Your credit score is the heavy lifter here. Data shows that 47.05% of Aussie applicants hold an excellent credit score, which allows them to access the most competitive car finance rates, often ranging between 6.59% and 9.95%. If your credit file is a bit messy, you might find yourself in the "bad credit" tier where average rates sit around 13.74%.

The asset itself also plays a massive role. A brand new ute or a green vehicle often attracts a lower rate because the resale value is predictable. Older vehicles are seen as higher risk, which is why a used sedan might cost more to finance than a shiny new showroom model. Lenders also look at your Loan-to-Value Ratio (LVR). Putting down a larger deposit reduces the lender's exposure, which can help you squeeze into a lower interest bracket. Employment stability is the final piece of the puzzle. While over 80% of successful applicants are in full-time roles, casual workers can still secure great deals by proving a consistent income history.

Most car loans are "secured," meaning the vehicle acts as collateral. This safety net for the lender is exactly why secured loans offer much lower car finance rates. If you are buying a much older vehicle that doesn't meet traditional security criteria, you might need an unsecured personal loan. These carry higher rates because the lender has no asset to claim if things go south. You can explore our vehicle finance options to see which structure fits your car best.

If you have an ABN, you might be eligible for commercial lending structures like a chattel mortgage. These often come with different rate tiers and potential tax benefits for business use. This is particularly common for tradies needing commercial finance for heavy machinery or trucks. A recent ASIC review of car finance highlighted the importance of transparency in these deals, ensuring providers focus on fair consumer outcomes rather than just high commissions. If you're ready to see what your profile can unlock, you can start your application online today.

Where you source your loan is just as important as the interest rate itself. Traditional Australian banks are often the first port of call, but their criteria can be incredibly rigid. While they offer the familiarity of a household name, their "one size fits all" approach means that if you don't fit a specific profile, you'll likely face a rejection or a higher rate. It is common to see establishment fees around $250 and monthly account charges of $15 tucked away in the fine print of these standard bank products, which quietly adds up over a five year term.

Dealership finance is the ultimate "one-stop-shop" convenience. You pick the car and sign the papers in one go. However, this ease often carries a premium. Dealers sometimes lead with a low headline rate while making their profit through higher vehicle prices or complex balloon structures. A specialised broker acts as your personal advocate, searching a wide panel of lenders to find the specific niche for your profile. This allows you to hunt for the most competitive car finance rates without racking up multiple hard credit enquiries that could damage your score.

Fees can turn a "cheap" loan into a financial headache. Beyond the interest, you need to watch for origination fees and early exit penalties. Some traditional lenders charge a $175 prepayment fee if you pay out the loan in less than two years. Balloon payments are another area where Aussies get caught out. They lower your weekly repayments, but you're actually paying interest on that large final sum for the entire life of the loan. It is vital to avoid hidden balloon payment traps that can wipe out your equity when you're ready to trade in.

If you're eyeing an electric vehicle, 2026 offers some of the best incentives in the market. Green car loans are currently the gold standard for low car finance rates. Specialised products, like those offered by BankWAW with rates as low as 5.54% for eligible EVs, are designed to incentivise the switch to hybrids and electric models. Understanding how the RBA influences interest rates helps you see why these green products are often more stable than standard personal lending. Ready to see what your profile can unlock? You can compare your personalised rates in minutes.

Getting a great deal shouldn't feel like a part-time job. We've stripped away the bureaucracy to make securing competitive car finance rates a fast, digital-first experience. Whether you're in Perth or Penrith, our national reach ensures you get the same expert care and access to a massive panel of lenders. We don't just look at numbers. We look at your goals. Our team handles the heavy lifting so you can focus on picking the right colour for your new ride. For readers seeking professional guidance on broader financial matters, you can discover Engage Financial Solutions and their approach to expert consultancy.

The process is designed to be punchy and professional. We know you want to get on the road, not sit in a bank manager's office. By using a specialised broker, you bypass the rigid "computer says no" attitude of traditional institutions. You can apply for your tailored rate today and see exactly where you stand without the typical finance-induced headache.

Many banks shy away from anything that isn't a standard sedan. We're different. We're experts in leisure assets, helping Aussies organise finance for caravans and motorhomes for that dream "big lap" around the country. If you're planning an epic road trip, check out The 2026 Guide to Caravan Finance for a deep dive into those specific requirements. For businesses, our commercial solutions allow you to scale your fleet or upgrade machinery quickly to meet market demand.

Speed is our specialty. To get the ball rolling, have your recent payslips, bank statements, and ID ready. Our experts take these documents and do the legwork immediately. We filter through hundreds of loan products to find the best car finance rates for your specific profile. We pride ourselves on a stress-free process that values your time. Why wait weeks for a bank's "maybe" when you could have a professional "yes" in a fraction of the time? It's about getting you moving sooner with total confidence.

You now have the tools to cut through the marketing noise and find a deal that actually works for your budget. Remember that the best car finance rates aren't found on a billboard; they are built on a solid credit profile and a loan structure that matches your specific asset. By looking past the headline interest rate and focusing on the comparison rate, you protect yourself from the sting of hidden fees and complex balloon payment traps.

We've spent years refining a process that puts your goals first. With access to a wide panel of Australian lenders and specialised expertise in car, caravan, and marine finance, we do the heavy lifting so you can focus on the drive. Our digital-first approach ensures a fast, stress-free approval process that gets you on the road or the water sooner without the typical bank-induced headaches. If you're a business leader wanting to bring that same level of positive energy to your workplace, learn more about Ocomedy Show and their professional humour-based engagement solutions.

Get a tailored car finance quote from the Motorlend experts

Your next adventure is waiting just around the corner. Let's get you there with a finance package that feels as good as the drive itself.

A good rate depends on your credit profile and the vehicle type, but for prime borrowers in July 2026, anything between 6.59% and 7.50% is considered highly competitive. If you're looking at an electric vehicle, specialised green loans can drop even lower, with some lenders offering rates around 5.54% for eligible models. Always check the comparison rate to ensure you're getting a true deal once fees are included.

No, a balloon payment doesn't lower your interest rate. It only lowers your monthly repayment amount by deferring a large portion of the loan principal until the very end of the term. Because you're carrying a larger debt for the duration of the loan, you'll actually end up paying more total interest over the life of the contract than you would with a standard principal-and-interest structure.

In many cases, yes. While a bank only offers its own rigid products, a broker has access to a wide panel of lenders and can find a specialised provider that fits your specific financial profile. This competition often leads to better car finance rates because the broker can "shop around" for the lowest offer without you having to submit multiple applications that could damage your credit score.

Your credit score is the primary tool lenders use to determine your risk level and set your personalised rate. Borrowers with an excellent score often secure rates under 7%, while those with a below-average history might see offers closer to the market average for bad credit, which sits around 13.74%. Keeping your credit file clean is the most effective way to drive down the cost of your borrowing.

Yes, many Australian lenders now offer discounted "Green Car Loans" specifically for electric and hybrid vehicles. These specialised car finance rates are often significantly lower than standard petrol or diesel loans to encourage the adoption of low-emission cars. Some of the most aggressive deals in the 2026 market are reserved exclusively for EV buyers, often sitting 1% to 2% below standard market rates.